Air cargo tonnages build ahead of Lunar New Year: WorldACD

Average worldwide rates of $2.33/kg are 20% below their elevated levels last year

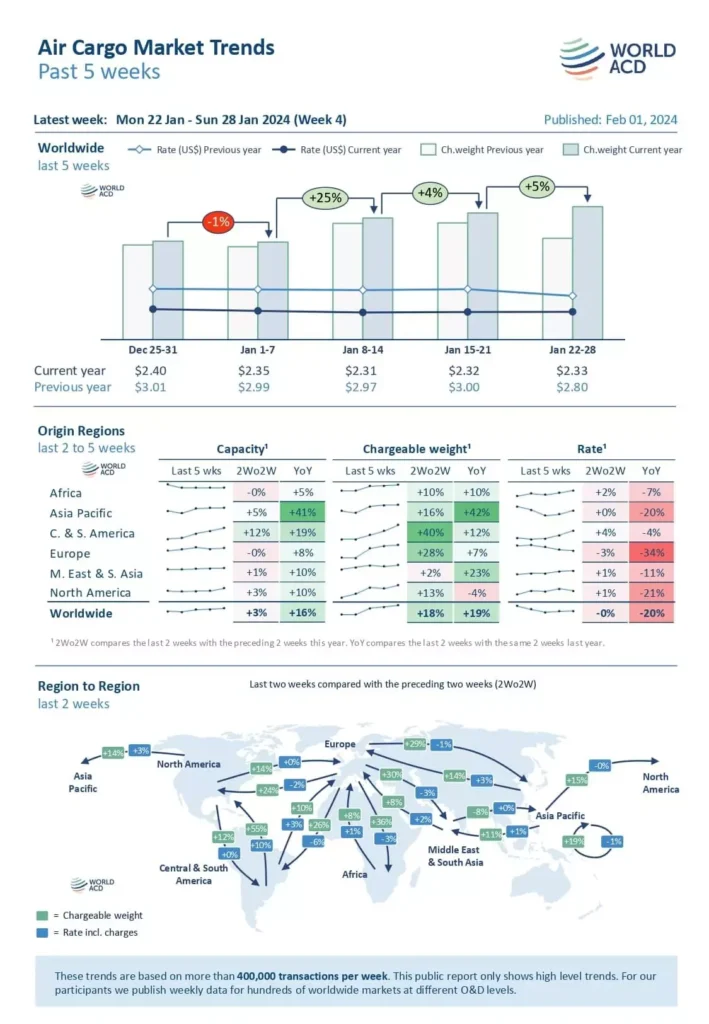

In the last full week of January, global air cargo volumes continued to surge, anticipating the Lunar New Year (LNY) on February 10. The data from WorldACD Market Data reveals that both the last two weeks and the entire month of January experienced significant increases compared to the same period last year. Preliminary figures for January show a 14 percent rise compared to January 2023, based on over 440,000 weekly transactions monitored by WorldACD. It’s important to note that last year, LNY fell on January 22, influencing the figures, as the week following LNY typically sees a drop in tonnages ex-Asia Pacific. However, a consistent upward trend in year-on-year tonnages has been observed for several months, driven by strong e-commerce demand, particularly ex-Asia Pacific since the final quarter of last year, along with a limited shift from sea freight to air and sea-air cargo in recent weeks due to disruptions in Red Sea container shipping.

In the weekly analysis, the initial figures for week 4 (January 22-28) indicate a further five percent increase in global air cargo tonnages compared to the previous week. This follows a 25 percent rise in week 2 and an additional four percent increase in week 3. Average global prices remained relatively stable throughout January at $2.33 per kilo, compared to around $2.60 in early to mid-December. The combined tonnages for weeks 3 and 4 show an 18 percent global increase compared to the preceding two weeks (2Wo2W), with average rates stable and capacity up by three percent. Outbound tonnages increased significantly from major global regions on a 2Wo2W basis, with double-digit percentage increases observed in Central & South America (40 percent), Europe (28 percent), Asia Pacific (16 percent), and North America (13 percent).

Most major intercontinental lanes recorded double-digit percentage increases in tonnages on a 2Wo2W basis, including a notable 55 percent surge from Central & South America to North America, driven by increased demand for Valentine’s Day flowers on February 14. Looking at the year-on-year perspective, global demand in weeks 3 and 4 combined is up by 19 percent compared to the equivalent period last year, with tonnages ex-Asia Pacific and ex-Middle East & South Asia up by 42 percent and 23 percent, respectively. Overall, worldwide air cargo capacity remains significantly higher than last year’s levels (16 percent), with a notable 41 percent rise ex-Asia Pacific. Although average worldwide rates of $2.33 per kilo in week 4 are 20 percent below their levels this time last year, they remain substantially above pre-Covid levels (+31 percent compared to January 2019).

Despite the uncertain outlook, freight and logistics experts anticipate a decline in air cargo’s recent boost from sea freight conversions after Lunar New Year. However, one major forwarder notes that the momentum in air cargo will persist, driven in part by ocean container equipment shortages at origin ports due to extended ocean shipping rotations around the Cape of Good Hope. As pressure on air cargo capacity increases, a corresponding rise in air cargo rates is expected in the coming weeks on specific trade lanes, as already observed in recent weeks.

February 9, 2024 - By :

February 9, 2024 - By :